This straightforward explanation of WIP inventory includes a step-by-step formula and explanation of the place of WIP inventory in the end-to-end supply chain.

This straightforward explanation of WIP inventory includes a step-by-step formula and explanation of the place of WIP inventory in the end-to-end supply chain.

Work in process (WIP) inventory is an important line item on a merchant’s balance sheet and a key indicator of the health of their supply chain. WIP inventory is not applicable to merchants who purchase finished goods from a supplier for resale. However, if your procurement process looks anything like the following three scenarios, you should be tracking and calculating your WIP inventory.

In all three of these scenarios, you have unfinished goods at some stage of the process that are considered WIP inventory. Continue reading to learn exactly what WIP inventory is, how to calculate it, why it matters, and how it fits into a healthy supply chain.

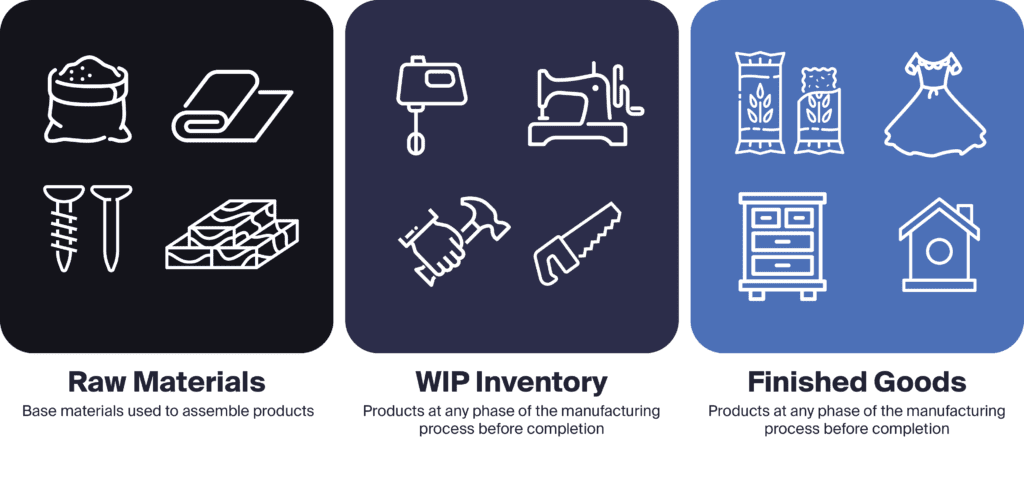

On any merchant’s balance sheet, the inventory line item is made up of three types of inventory:

So for the purposes of accounting, WIP inventory is the total value of any unfinished goods, and although they can’t be sold, these goods are counted as an asset on a balance sheet. It’s important to include WIP inventory as an asset when calculating the value of your business for finding investors or securing financing. On the accounting side, calculating WIP inventory is also important for understanding the true value of your inventory for tax purposes.

However, calculating WIP inventory is also important for understanding the health of your business’s supply chain and optimizing your supply chain planning. Generally speaking, it’s considered best practice to carry as little WIP Inventory as possible. Having too much WIP inventory on-hand can be an indication of bottlenecks in your manufacturing or procurement process.

Most merchants calculate their WIP inventory at the end of a reporting period (end of quarter, end of year, etc.), and are looking for their “ending WIP inventory”. To calculate ending WIP inventory, you need beginning WIP inventory, which is the previous reporting period’s ending WIP inventory.

You must also calculate the production costs that are currently tied up in unfinished inventory. This includes the raw materials and the labor and overhead costs associated with the percentage of work that has been completed.

Finally, you need the value of your finished goods, which is the total value of your inventory ready to be sold. It includes manufacturing costs, raw materials, and overhead costs.

Once you have all of these variables determined, the formula for WIP inventory is as follows:

WIP Inventory Example:

For example, if your business is calculating WIP inventory at the end of each quarter, and your accounting records show that your ending WIP inventory previous quarter was $15,000, that will be your beginning WIP inventory for the current quarter.

Then you find that you have invested $225,000 in production costs for the quarter, and the total value of your finished goods is $215,000.

In this example, you would calculate your ending WIP inventory as follows:

($15,000 + $225,000) – $215,000 = $25,000

Although WIP inventory cannot yet be sold, it’s considered an asset on a merchant’s balance sheet. For this reason, it’s considered best practice to hold as little WIP inventory as possible. In fact, an excess of WIP inventory can be a symptom of bottlenecks within the supply chain. Having excess WIP inventory on-hand can also raise operating costs and reduce productivity in the following ways:

It’s particularly important to monitor supply chain efficiency in a time of unprecedented supply chain disruptions leading to raw material shortages and extended lead times. These elevated lead times have led many merchants to forecasting demand and procuring inventory 6 months in advance (as opposed to historically forecasting on a quarterly basis). To avoid a buildup of WIP inventory, it’s important to work closely with suppliers for the most accurate projections of lead times possible.

Another important factor in keeping WIP inventory low is accurate inventory cycle counts enabled by an integrated Warehouse Management System (WMS). Having accurate, real-time inventory counts enables for more accurate forecasting to make communicating with suppliers and freight forwarders easier and more efficient. Outsourcing fulfillment to a 3PL or 4PL can give small to mid-sized merchants access to enterprise-level inventory management systems to optimize their WIP inventory flow.

What is included in work in process inventory?

Work-in-process costs include all raw materials and labor needed to manufacture the final product. Calculating WIP inventory is complicated because it requires an assessment of the cost of labor and overhead associated with the percentage of work completed. Because it is difficult and time consuming to calculate, most merchants try to have as much inventory as possible in the finished goods state before the end of a reporting period.

How do you calculate work in process inventory?

There are three variables you need to calculate work in process inventory:

Once you have all three of these variables, the formula for calculating WIP inventory is:

(Beginning WIP Inventory + Production Costs) – Finished Goods = Ending WIP Inventory

How do I account for work in progress inventory?

Works in process (WIP) are included in the inventory line item as an asset on your balance sheet. The two other categories of inventory are raw materials (the beginning materials used to manufacture a product) and finished goods (fully assembled products ready to be sold).